Navigating the Challenges of Wildfire Risk Modelling

Next-Generation Solutions Needed for Rapidly Evolving Peril

As wildfires raged across Northeastern Canada in June, spreading toxic smoke across a large swath of Eastern and Central U.S., risk and insurance executives were reminded of the myriad challenges associated with wildfire risk.

Only a few weeks earlier, in April, Southern California experienced its first wildfire of 2023 when 130 acres of San Bernardino forest burned in an hour. Subsequently, State Farm and Allstate announced they will no longer write homeowners policies in California as wildfire threats become increasingly dangerous, difficult to predict, prepare for and manage.

Not surprisingly, eight of the 10 costliest wildfires in U.S. history listed by the Insurance Information Institute occurred in the past six years. From a safety, risk management, and insurance perspective, wildfire continues to be a growing and evolving peril, particularly across California, the Western U.S., and Canada, as well as in South America, Australia/New Zealand, and parts of Europe and Africa.

One of the most daunting underwriting challenges in managing wildfire risk is that there are currently no market-accepted models to evaluate the frequency and severity of wildfires. Approaches used in traditional exposure models, such as those for windstorms and floods, have not proven to be very effective for wildfire risk.

At the same time, there are many insurance providers delivering solutions based on location-level imagery and AI-based risk scores. However, overly simplistic “scoring” of the risk hides the nuances and specific variables contributing to wildfire risk that are necessary to facilitate informed underwriting decisions. They also do not equip brokers with the evidence needed to negotiate on behalf of clients in wildfire-prone regions and to make the case that they may still qualify for insurance. As a result, an otherwise “insurance-worthy” client remains uninsured – and all parties lose.

On a macro scale, the California actions taken by two leading insurers are emblematic of the outcome: The inability to evaluate and price risk, leading to coverage gaps – not to mention, completely uninsured exposures – for risk owners as well as lost opportunities for insurers and brokers.

Finding a Way Forward: Building Next-Generation Models for Wildfire Risk

Despite the various challenges in creating meaningful approaches to model wildfire exposure, new tools for capturing and analyzing data from multiple sources are leading to new solutions.

One key is to provide transparency into the multiple variables that drive wildfire risk as well as how each variable increases wildfire hazard exposure or affects resilience for a particular property. Today, there are reliable methods to capture data needed for assessing climate, topography, and fuels, all of which have significant impacts on wildfire risk at specific locations.

The next generation of models must consider time dimensions, such as fuel height changes over time, including regrowth of vegetation in burn areas. To be as accurate as possible, models must be updated at least annually. Notably, many aspects of wildfire-related exposures, such as stock throughput, rely on timing over the course of the year. In addition, models should be calibrated based on climate conditions over time. Models should simultaneously consider historical climate data over a significant period of time (30 years) and provide additional weight for abnormal weather conditions in the previous year.

In modeling wildfire risk going forward, geo-visualization becomes key. This enables users to gain context around numbers generated and literally to see the variability of risk in the vicinity of a property. All of this should be validated using the latest high-resolution imagery of buildings and surrounding areas.

Finally, the models also need to consider the vulnerability or resilience of a property, including fireproof construction, fire protection systems, available water supplies, and firefighting response resources, surrounding buildings and their construction, as well as natural and man-made barriers to fire spread.

Although drought and other climate conditions are exacerbating and expanding the risk of wildfires around the world, the next generation is delivering reliable models. The ability to capture a wide range of relevant exposure-related data and to assess it in a granular way through artificial intelligence and data science may help facilitate more effective insurance underwriting, as well as inform related risk mitigation measures, disaster response, and crisis management.

# # #

About Teren

Denver-based Teren is a leading climate resilience data and analytics company. By harnessing the plethora of remotely sensed data from orbit and airborne platforms, Teren delivers hyper-localized, asset-level insights for managing climate risk and building resilience over time. Teren uniquely solves complex problems by applying modern data science techniques, geo-intelligence, and high-performance computing to deliver timely, actionable results. Teren works with asset owners, developers, engineering firms, and insurers to pinpoint risk, reduce exposure and improve climate resilience. Visit https://www.teren4d.com.

About EigenRisk®

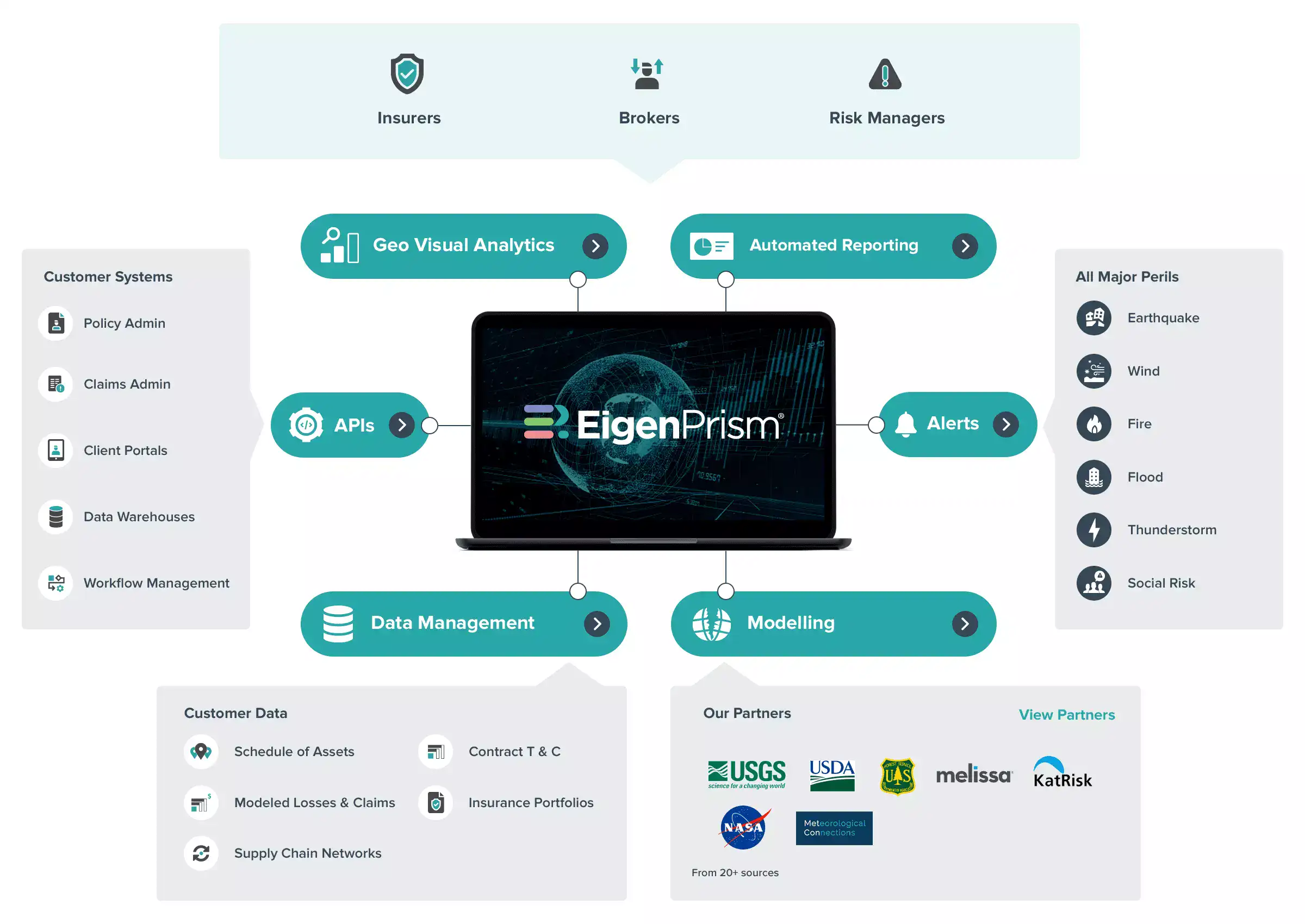

EigenRisk, Inc., an independent insurance technology firm, helps (re)insurers, brokers, and risk managers across the globe manage catastrophe risk, and drive higher growth, customer engagement, and operational efficiency. The firm’s cloud-based platform provides one-stop access to powerful data management, geo-visualization, analytics, reporting, modeling, alerts, and APIs. These capabilities are integrated with hazard data, event projections, and simulations curated from more than 20 leading public and private sources to provide a more dynamic and complete perspective of risk. Visit www.eigenrisk.com.

{kind=link}